Every year around October, my patients start checking their mailboxes with a mix of excitement and anxiety. They are looking for the official letter from the Social Security Administration. They want to know the “COLA” the Cost-of-Living Adjustment.

As a doctor, I see how this one number dictates the quality of life for millions of American seniors.

It determines if you can afford that extra grocery trip or if you have to tighten your belt even further. But there is a silent partner in this equation: Medicare.

For most people, your Social Security check and your Medicare Part B premium are tied together. When one goes up, the other often follows.

Let’s break down what 2026 looks like for your wallet and how these two systems dance together.

What Exactly is the COLA Adjustment

Think of the yearly benefit adjustment as a way for your bank account to keep its head above water. It is not some fancy gift or a bonus from the government; it is just a tool to help your money survive when things like eggs, milk, and gas keep getting more expensive.

If everything you buy is costing more, it only makes sense that your benefits should grow a little bit to match.

In 2026, even though the economy is finally starting to feel a bit more stable, we all know that a simple trip to the grocery store still feels much pricier than it did a few years ago.

Because of this, current projections suggest the 2026 increase could be around 2.8%. While this extra cash is a big relief for many of my patients, I always tell them to stay cautious.

It is very easy for that small boost to disappear quickly if you fall into 3 common Medicare enrollment mistakes that can lead to unexpected bills and penalties.

How Medicare Part B Actually Impacts Your Monthly Check

If you’re like most of the patients I see in my clinic, you probably never actually write a check for your Medicare Part B premium.

Instead, the money is taken out before your Social Security benefits even hit your bank account. While this “set it and forget it” system is convenient, it often leads to a lot of confusion when January rolls around.

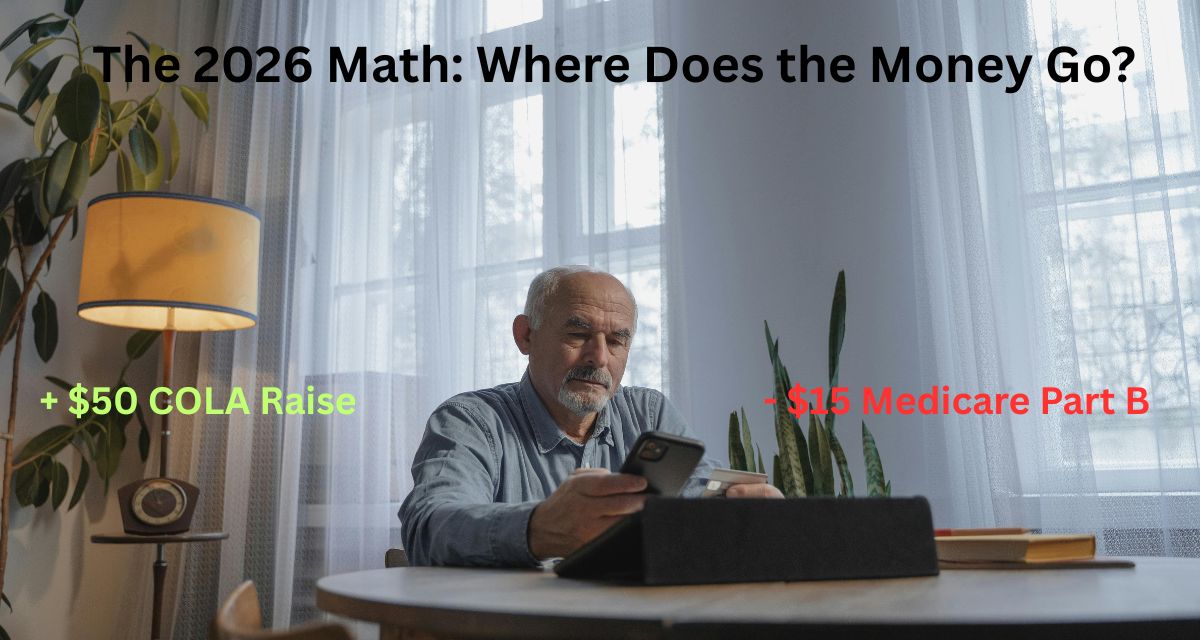

Here is the reality: When Medicare announces a premium increase for 2026, that extra cost comes directly out of your Cost-of-Living Adjustment (COLA).

Think of it this way:

If your Social Security benefit goes up by $50 because of inflation but Medicare raises the Part B premium by $15 at the same time then your actual raise is really just $35.

It is simple math but it can feel like a punch in the gut if you aren’t expecting it.

I spend a lot of time talking with patients who feel frustrated or even cheated when that first check of the year arrives.

They see a smaller number than they were promised in the news and they feel like they lost out.

I am sharing this so you aren’t caught off guard when 2026 starts. When you know exactly how these two numbers work together you can plan your monthly budget without any nasty surprises or sticker shock in January.

The “Hold Harmless” Provision Explained

There is a very important rule that every senior should know about, called the “Hold Harmless” provision.

This is a law that protects you from your Social Security check actually going down because of Medicare.

If the Medicare premium increase is larger than your Social Security COLA increase, the government cannot lower your net check. They will only take as much as your COLA increase allows, leaving your check at the same dollar amount as the year before.

This protection is a safety net. It ensures that no matter how much healthcare costs rise in 2026, your basic income from Social Security remains stable.

As a medical provider, I find this rule gives my patients a lot of peace of mind during uncertain economic times.

How to Plan for Your Actual 2026 Income

Once the official numbers come out in late 2025 you should sit down and look at your net income. This is the actual amount of money that lands in your bank account every month.

I always tell my patients to take whatever extra money they get even if it is just 20 or 30 dollars and put it into a small medical emergency fund.

Healthcare always has a way of throwing surprises at you like a co-pay for a specialist or a new medication that isn’t fully covered.

When you look at your Social Security and Medicare as one single unit you can stop worrying about hidden deductions.

It helps you stay in charge of your own retirement instead of just waiting to see what happens to your check.

Why Your Income History Still Matters

Even with COLA adjustments, your past income can still affect your 2026 Medicare costs through something called IRMAA (Income-Related Monthly Adjustment Amount).

If you had a high-earning year two years ago—perhaps you sold a house or took a large 401k withdrawal—Medicare might charge you more for your premiums, regardless of what the COLA says.

If you get a letter saying your premium is higher than your neighbors’, don’t panic. Check your tax returns from two years ago. If your life has changed (like you’ve fully retired), you can often ask for a “Life Changing Event” adjustment to bring that cost back down.

Will Your COLA Raise Be Eaten by Medicare?

Usually when Social Security benefits go up Medicare Part B premiums follow right behind.

Since these premiums are taken out of your check before you even see it you might feel like you aren’t getting much of a raise at all.

It can be frustrating to see a cost increase take away the extra money you were counting on for groceries or bills. But there is a bit of good news that most people don’t know about.

There is a rule called the hold harmless provision that protects you.

This law basically says that a Medicare premium hike cannot make your Social Security check smaller than it was the year before. It is a safety net that ensures your take home pay stays stable even when healthcare costs go up.

Final Thoughts from the Doctor’s Office

Financial health is a vital sign, just like your heart rate or blood pressure. When your income is stable, you make better health choices.

You buy fresher food, you stay active in your community, and you don’t skip your medications.

The 2026 COLA and Medicare updates are tools to help you navigate your senior years with dignity.

Stay informed, read the notices from Social Security carefully, and never hesitate to ask for help if the math doesn’t seem to add up.

Frequently Asked Questions!

When will the official 2026 COLA be announced?

The Social Security Administration typically announces the COLA for the upcoming year in mid-October. This is based on inflation data from the third quarter of the year.

Can my Medicare premium ever be more than my Social Security check?

No. For the vast majority of seniors, the “Hold Harmless” rule prevents Medicare premiums from exceeding the amount of your Social Security increase, ensuring your check doesn’t decrease.

Does COLA affect my Medicare Advantage (Part C) premiums?

Not directly. COLA is tied to Part B premiums. Medicare Advantage plans set their own monthly premiums, though many plans in 2026 are moving toward $0 premiums to stay competitive.

Why did my neighbor get a bigger Social Security raise than I did?

COLA is a percentage, not a flat dollar amount. If your neighbor has a higher monthly benefit, their percentage-based increase will result in more dollars added to their check.

Will my 2026 COLA be taxed?

It depends on your total “combined income.” If you and your spouse earn above a certain threshold, a portion of your Social Security benefits (including the COLA increase) may be subject to federal income tax.

Dr. Neelam Tahir is a dedicated medical professional (MBBS) with a passion for helping seniors navigate the complex world of Medicare. With years of clinical experience, she specializes in simplifying healthcare benefits, from Part B givebacks to healthy food allowances. Her mission is to ensure that every senior has access to the expert guidance they need to live a healthy and financially secure life