Have you ever picked up one of those thick Medicare handbooks and felt your head start to spin? Honestly, it feels like they’re written in a different language sometimes.

If you’ve ever looked at those brochures and felt completely overwhelmed, I want you to know something: You are not alone.

In my clinic, I see this every single day. A patient will sit across from me, sigh deeply, and pull out a crumpled envelope or a glossy flyer.

They usually look at me with so much frustration and ask, “Doc, please just tell me… what on earth is Medicare Part C? Do I even need this, or is it just more paperwork for me to worry about?”

Look, I get it. Life is busy enough without having to become an insurance expert.

So, let’s do this: forget the medical jargon and the confusing “insurance-speak” for a minute. Take a deep breath.

I’m going to explain this to you exactly how I’d explain it to my own mom or a close friend over a cup of coffee.

Just the simple, honest truth. We’re going to talk about how this works and, more importantly, how it might actually put some money back in your pocket when you’re standing at the pharmacy counter.

So, What Exactly is Medicare Part C?

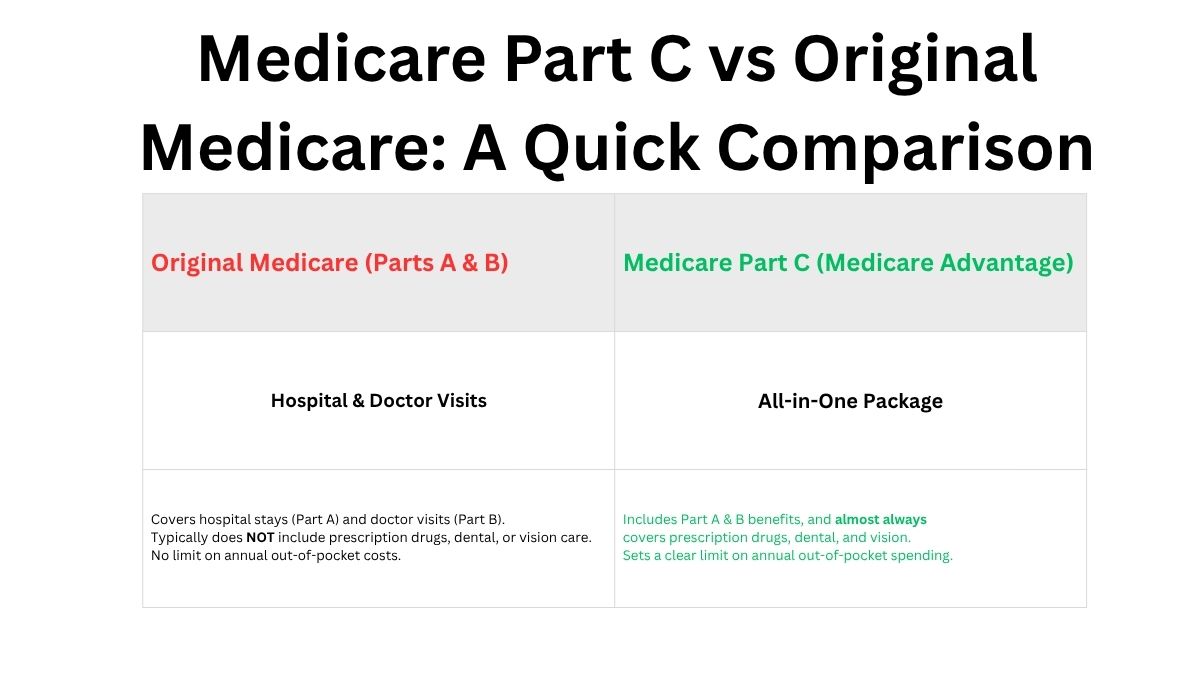

Think of “Original Medicare” (Parts A and B) as buying pieces of a puzzle.

You get your hospital coverage here, your doctor visits there, and then you have to go find a separate plan for your drugs. It’s a lot to keep track of!

Medicare Part C, which most people call Medicare Advantage, is like getting the whole puzzle already put together in one box.

It’s a “combo plan” offered by private companies that Medicare approves.

Instead of having three different cards in your wallet, you just have one. It covers your hospitals, your doctors, and the best part, it almost always includes your Prescription Drug Coverage (Part D) as well.

Why Do I Call it the “All-in-One” Plan?

It’s not just about the basics, either. Most of these plans throw in those ‘extra’ bits that Original Medicare tends to ignore.

I’m talking about things like getting your teeth cleaned or getting a new pair of glasses without paying the full bill yourself.

Some of my patients even use the fitness memberships, like SilverSneakers, to stay active, which is something I always encourage as a doctor

How Medicare Part C Saves You Money on Prescriptions

Now, let’s talk about the part that keeps most of my patients up at night: the pharmacy bill. It’s a bit of a shock, but Original Medicare basically leaves you out in the cold when it comes to prescriptions.

You’re usually stuck buying a whole separate plan just to cover your meds.

But with Medicare Part C, it’s a totally different world because the drug coverage is already tucked inside the plan.

I’ve had so many people sit in my office and literally blink in surprise when they find out they don’t have to pay an extra monthly premium just to have that coverage.

It’s one of those small wins that actually makes a difference in your monthly budget. And it doesn’t stop there.

Because these plans partner with specific pharmacies, I’ve seen my patients walk away paying just a couple of dollars for their blood pressure or cholesterol pills. It’s a far cry from the full-price nightmare many are used to.

But if you ask me what the real ‘secret weapon’ is, it’s the safety net they build in.

We call it the out-of-pocket limit, but I just call it ‘peace of mind.’ In Original Medicare, your bills can just keep stacking up forever.

But with Part C, once you hit a certain limit, the plan finally says, ‘Okay, we’ve got it from here,’ and they cover the rest for the year.

That’s the kind of protection that keeps a sudden illness from turning into a financial disaster

A Real Example from My Clinic

Take my patient, Mrs. Gable, for example. She was terrified that she’d hit a “spending gap” and wouldn’t be able to afford her insulin by the end of the year.

When we looked at a Part C plan together, she saw that her insulin copay stayed flat and predictable.

The relief on her face was huge. For her, it wasn’t just about the money, it was about knowing she could actually afford her medicine every single month without fail.

Is Medicare Part C Really the Right Fit for You?

I always tell my patients the same thing: there is no such thing as a perfect plan. There is only the right plan for you and your specific health needs.

Before you sign up for any Medicare Advantage plan, you need to slow down and think about your own life. For example, think about your doctor.

If you’ve been seeing the same doctor for 20 years and you trust them with your life, you have to make sure they are “in the network.” Most Part C plans have a specific list of doctors they work with. I’d hate for you to switch plans only to find out your favorite doctor doesn’t accept it.

Then, there is the matter of your medications. Every plan has its own “Formulary,” which is just a fancy word for a list of drugs they agree to pay for.

If you take a specific, expensive brand-name drug, you must check if that plan covers it. A “cheap” plan can become very expensive very fast if it doesn’t cover the one pill you need every day.

You also have to think about your lifestyle. Do you spend six months in Florida and the rest of the year in New York? If you travel a lot, a local Part C plan might feel a bit restrictive.

Their networks are often tied to where you live. If you’re across the country and need a non-emergency checkup, you might find yourself paying more than you expected.

My best advice from the clinic? Please, don’t just pick a plan because of a flashy TV commercial or a celebrity spokesperson. Those ads aren’t looking at your pill bottles—but you should be. Real savings happen when the plan matches your actual prescriptions and your actual doctors.

Final Thoughts from Dr. Neelam

At the end of the day, understanding what is Medicare Part C is all about knowing your options.

It’s about making sure you get the dental, vision, and drug coverage you deserve without breaking the bank.

If you are tired of carrying around three different insurance cards and paying multiple bills, Part C might be the breath of fresh air you need.

Frequently Asked Questions (FAQs)

If I join Medicare Part C, do I lose my Original Medicare?

Not at all! Joining Part C means you are still very much in the Medicare program.

Instead of the government, a private insurance company simply manages your benefits for you. Rest assured, all your original Medicare rights and protections remain exactly the same

Wait, can I still see my favorite doctor with Part C?

Usually, no. Most Part C plans have a specific network of doctors and hospitals. If you see a doctor “out-of-network,” you might have to pay more, or the plan might not cover it at all. Always check the directory first!

Does Medicare Part C cover dental, vision, and gym memberships?

Yes! This is one of the biggest “perks.” Most plans include routine dental cleanings, eye exams, and even “SilverSneakers” fitness programs at no extra cost to you. Original Medicare does not offer these.

What happens if I move to a different state?

Since Part C plans are tied to a specific service area (usually your county), you will likely need to switch to a new plan that is available in your new location. You get a “Special Enrollment Period” to do this so you don’t lose coverage.

Is Part C the same as a “Supplement” or “Medigap” plan?

This is the most common confusion! No, they are opposites. A Supplement plan pays “after” Medicare pays. Part C “replaces” how you receive your Medicare altogether. You cannot have both at the same time—it’s one or the other.

Medical Disclaimer:

I am a doctor, but I am not an insurance agent. This article is for educational purposes only. Medicare plans change every year and vary by location, so please consult with a licensed professional or visit Medicare.gov before making any final decisions.

Dr. Neelam Tahir is a dedicated medical professional (MBBS) with a passion for helping seniors navigate the complex world of Medicare. With years of clinical experience, she specializes in simplifying healthcare benefits, from Part B givebacks to healthy food allowances. Her mission is to ensure that every senior has access to the expert guidance they need to live a healthy and financially secure life